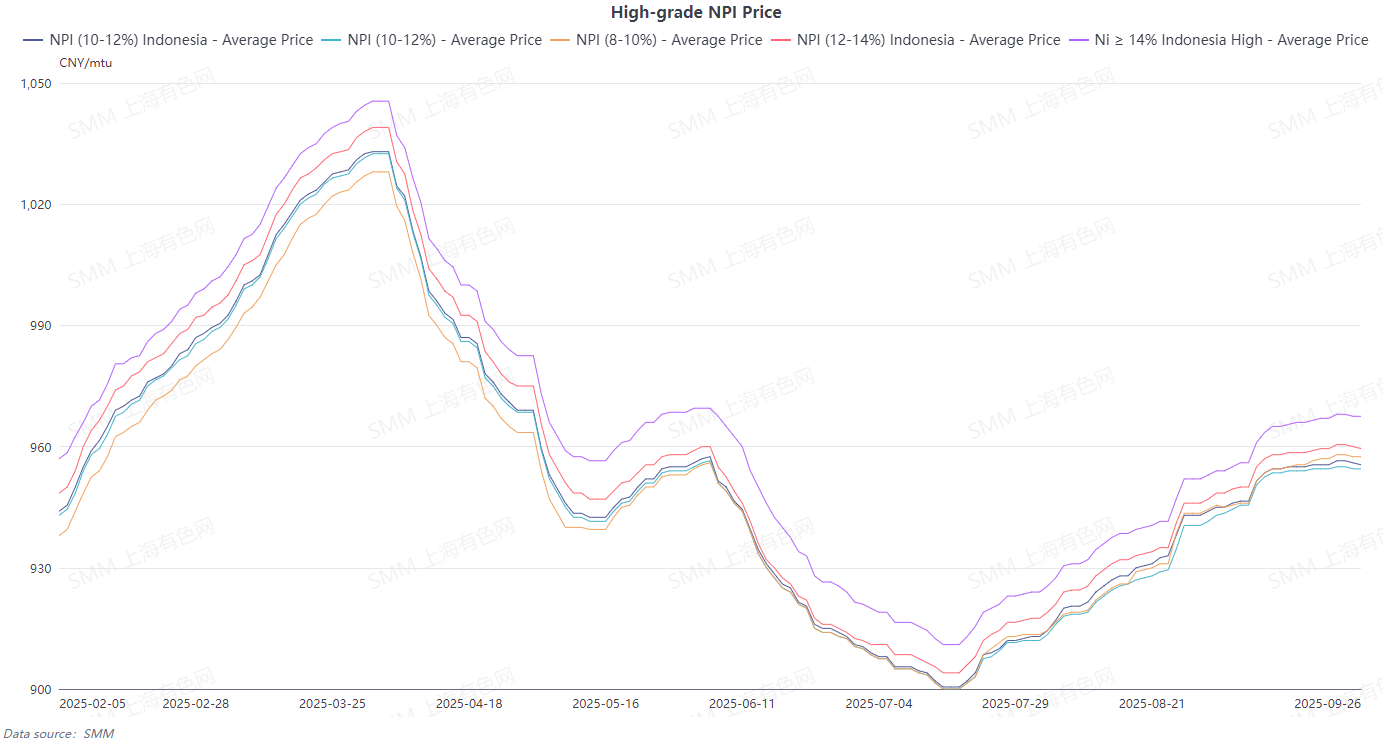

The SMM average price of 10–12% high-grade NPI increased by 0.5 yuan/mtu WoW to 954.7 yuan/mtu (ex-factory, tax included), while the average Indonesia NPI FOB index price remained flat WoW at $117.44/mtu. This week, high-grade NPI prices began to decline after a period of stalemate.

Supply side, although still in the traditional peak season with firm cost support, downstream procurement remained sluggish, upstream enterprise inventory increased, and the willingness to refuse to budge on prices weakened to some extent. Demand side, the destocking speed of stainless steel social inventory slowed down, stainless steel enterprise profit margins remained under pressure, purchase willingness was weak, and low-price transactions emerged in some regions, dragging market prices to turn downward. Overall, peak season support is fading, trading sentiment is under pressure, and the high-grade NPI market has shifted to trading pessimistic expectations for future fundamentals, with prices starting to turn downward. High-grade NPI prices are expected to maintain a slight decline around the National Day holiday.

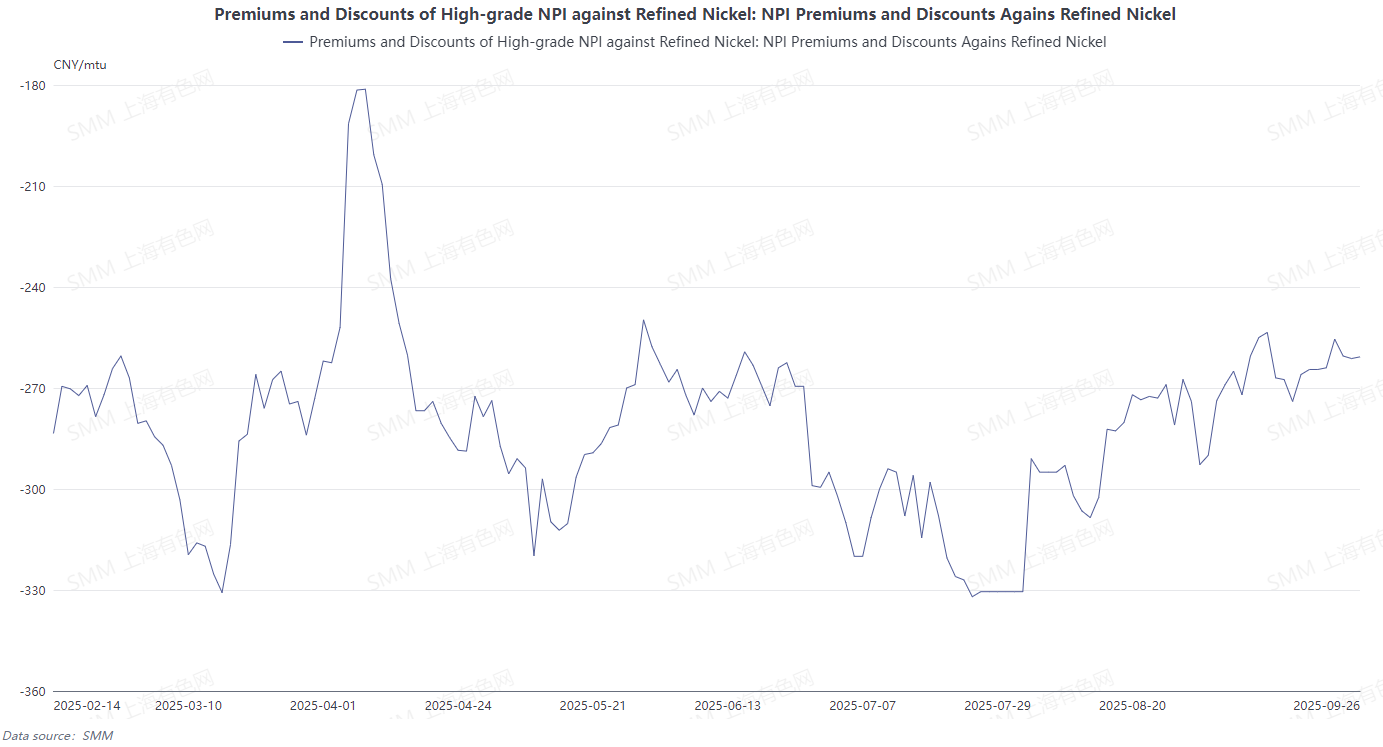

From the perspective of conversion of NPI to high-grade nickel matte, refined nickel prices rose significantly this week driven by disruptions at Indonesian copper mines, then pulled back to erase gains, with the average price ultimately remaining basically stable. High-grade NPI prices were also basically stable, and the average discount of high-grade NPI to refined nickel narrowed to 260.4 yuan/mt this week. Refined nickel prices are expected to remain flat next week, while high-grade NPI prices are projected to drop back slightly. The average discount of high-grade NPI to refined nickel may widen somewhat but remain within 300 yuan/mt, and the proportion of NPI converted to high-grade nickel matte is expected to be limited.

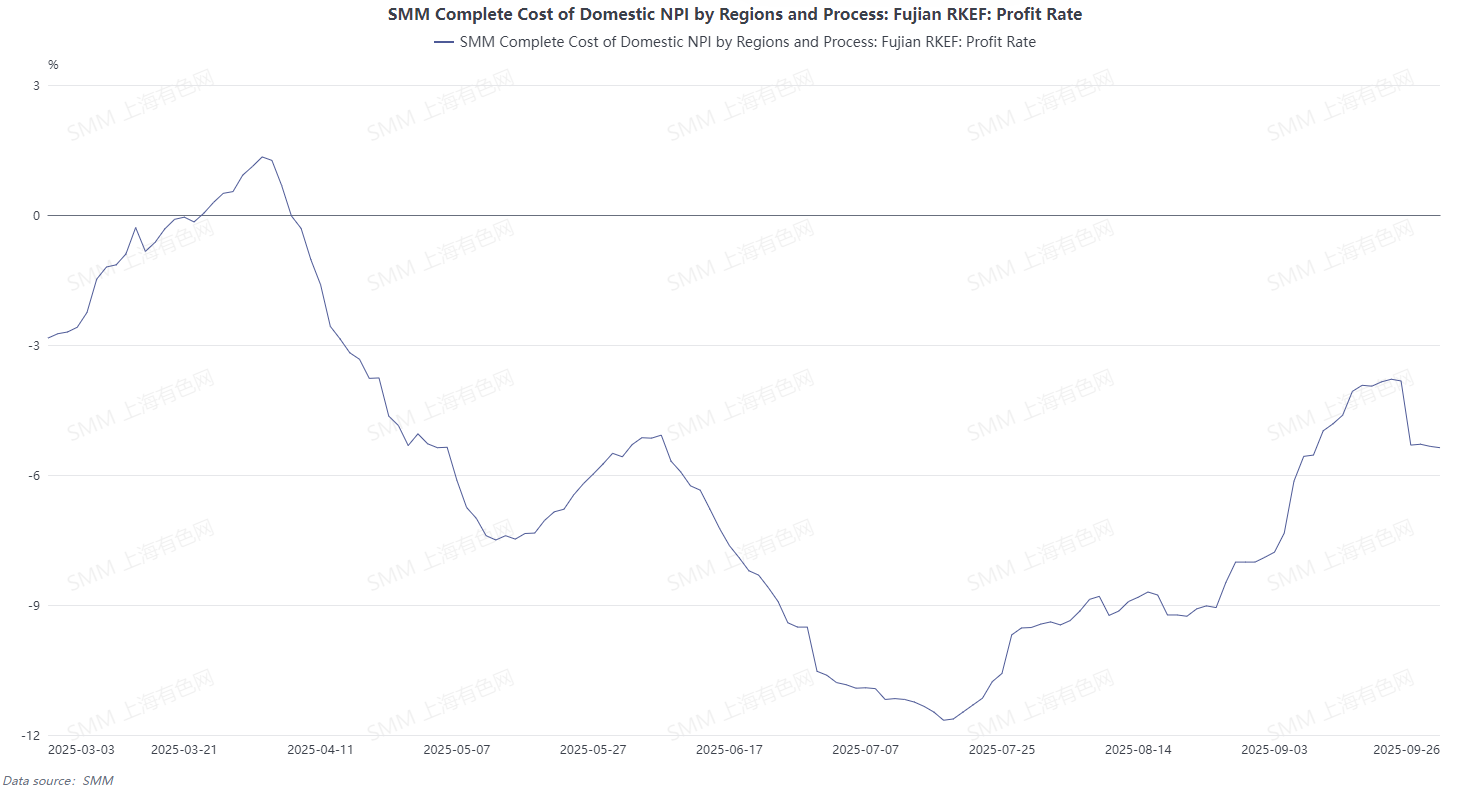

Cost side, based on the nickel ore prices calculated 25 days ago for high-grade NPI cash cost, high-grade NPI smelter profits declined this week. Raw material side, ore prices remained stable, but coking coal and coke prices rose significantly, and summer electricity prices also increased, driving costs upward. Meanwhile, high-grade NPI prices fell. Looking ahead to next week, auxiliary material prices on the raw material side are expected to remain high, while ore prices are projected to hold steady. With high-grade NPI prices under pressure, smelter profits are expected to continue declining.